Have you ever found yourself wondering whether or not to take up a new project or venture? How difficult has it been to make that choice for your business?

One way of making these decisions easier is by evaluating your past investment decisions. The results of your decisions will give an indication as to which aspects you need to focus on more, which ones you can go ahead with and also what kind of ventures that you should avoid. There are three methods that are used to compare the benefits of investment decisions.

The first is the Payback Period which is the time taken to recover the cost of an investment. Payback Period is considered to be the easiest means of evaluation. Let’s take an example to examine this concept further. Imagine Mr. Silva wants to invest in a solar panel system for his business. We all know solar panels cost a fair amount of money. However, for the sake of the example let’s say they cost 12,000 LKR. After Mr. Silva calculated the savings from the electricity bill he would get after this investment, he found out that he is saving 1,000 LKR per month. So to simply put, the Solar Panels would cover their initial cost in twelve months right? (1,000×12). That is the Payback period of those Solar Panels; 12 months, or 1 year, after which point the 1,000 LKR saved each month is pure profit.

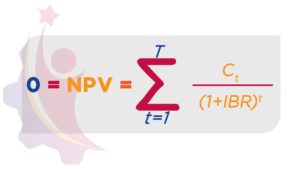

The next method is Net Present Value (NPV), which is the value, in today’s money, of an investment’s return by a given date, less the cost if the investment, which is of course already in today’s money. This is actually a bit harder to analyze than it sounds, and that is because of inflation and interest rates. In the current context, a 1,000 LKR note is worth 1,000 LKR. However, in another year, the value of that 1,000 LKR is not the same as it was before. I’m not saying that the 1,000 Rupee note you have hidden away in your wallet will magically turn into a 500 Rupee note or anything. It is just that the amount of goods and services you can buy with the note will eventually decrease compared to what you could buy today, due to the continuous increase in prices. NPV adjusts the return of investment according to the inflation factor and checks whether you would have earned more than what you spent, by the time you reach the end of the useful life of your investment. How do we calculate this? It has quite a complicated formula. However, you can easily find an online NPV calculator and enter your investment details in there to see if your investment is viable. Spreadsheets also now have built-in formulae to let you calculate NPV far more easily that it used to be possible, and you can experiment with your numbers when they’re set up in a spreadsheet. Your project will be more successful the higher an NPV figure you end up with. If I am to take Mr. Silva, his investment has a monthly return of 1,000 LKR right? Let’s say the monthly inflation rate is 10% (this is an artificial example, of course!) and the solar panels can only be used for 10 months. Let’s calculate.

Cost : 12,000LKR

So, the value of his return is decreasing by 10% every month.

Month 1 = 1000

Month 2 = 900

Month 3 = 800

Month 4 = 700

Month 5 = 600

Month 6 = 500

Month 7 = 400

Month 8 = 300

Month 9 = 200

Month 10 = 100

Total Return after adjusting inflation = 5,500

Profit / Loss = 5,500-12,000 = -6,500

Therefore, the NPV of this investment is negative, and it is not a suitable investment. Consider that the above example is a very simple calculation of NPV and there are a lot more factors involved when calculating in a real life scenario.

The third method is Internal Rate of Return (IRR), which gives an indication of what return you will receive on your initial investment with the assumption that the net present value is zero in the following equation. This in fact, with a tiny change, is the same equation we use to calculate NPV. It should be noted that in modern finance NPV is considered a superior method to assess projects compared to IRR.

The IRR calculation (modern spreadsheets will calculate it for you) tells you the discount rate at which NPV becomes equal to zero for the project you are assessing. Generally speaking, the higher the internal rate of return, the better the expected return from your project you can expect.

Did this discussion leave you confused? if not, you’re a CFO in the making! It is okay to be a little confused. These are complex theories. Go ahead and do an online search and read more. Find out more measures and online tools that will do the job for you and always, always, always plan your investments based on facts, and considering all scenarios.